distinguish between fixed capital and fluctuating capital account on the basis of credit balance

Partners’ Capital Accounts: In a partnership firm, separate Capital Accounts are maintained for each partner as each of the partners is the owner and has separate transactions with the firm. These Partners’ Capital Accounts can be maintained by following any of the 2 methods:

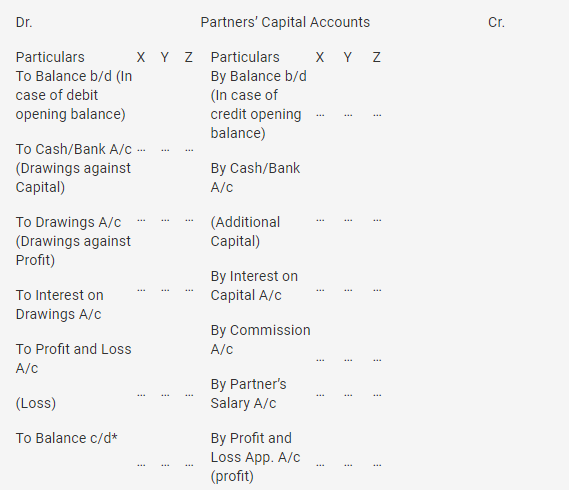

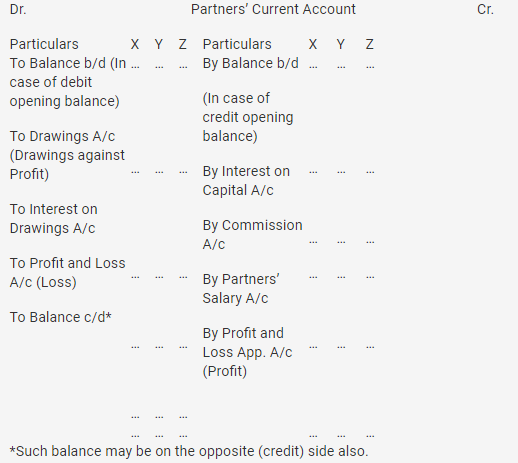

- Fixed Capital Accounts Method: In this method, the capital amount invested by each of the partner in the firm remains fixed or unaltered, unless a partner introduces additional capital or withdraws out of his or her capital. Such fixed capital is recorded in the Capital Account and for recording all transactions other than transactions related to capital such as drawings, interest on capital, interest on drawings, salary, commission, share of profit/losses, etc. Current Accounts are maintained in addition to the Capital Accounts.

Specimen for the 2 accounts maintained under Fixed Capital Method is as follows:

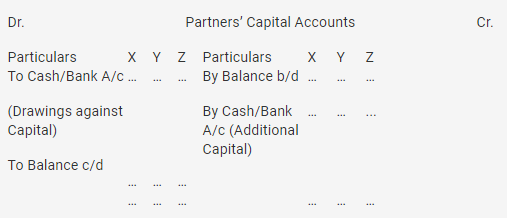

- Fluctuating Capital Accounts Method: In this method, only one account is maintained which is the Capital Account. All the transactions related to the addition or withdrawal of capital, salary, commission, interest on capital, interest on drawings, share of profits or losses, etc. are recorded in this Capital Account only. This method is followed for maintaining Capital Accounts and therefore, in the absence of any instructions, this method should be followed for maintaining the Partners’ Capital Accounts.

Specimen for the account maintained under Fluctuating Capital Method is same as follows: