The control process involves initially establishing standards and thereafter measuring and comparing performance’. Discuss these three steps in detail.

or

ABC Ltd wants to expand its product line. But for its effective working, they need to follow certain steps. State these steps.

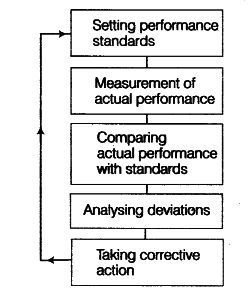

The main steps in controlling process are:

1.Setting Performance Standards

Standards are the criteria, against which actual ’ performance would be measured. These serve as benchmarks, towards which an organisation strives to work.

The first step of the control process is to establish standards, against which actual results are to be evaluated. Standards are set in quantitative as well as qualitative terms. But, managers should try to set standards in quantitative terms, which can be easily measured and compared later on.If standards are set in qualitative terms, an effort must be made to define them clearly for easy measurement. Due to changes taking place in internal and external environment, standards need to be revised regularly.

2. Measurement of Actual Performance

Once the standards are fixed, the next step is to measure the actual performance. Generally, it is conducted by the managers to analyse the overall efficiency level of the employees. While measuring the performance, objective and reliable methods should be used, such as sample checking, preparing reports, personal observation, etc.

Measurement should be done after the task is completed. However, sometimes performance can be measured during the performance to ensure regular control over the activities. Usually, in large organisations, certain pieces are checked at random, instead of checkisg the whole lot. This is called sample checking.

2. Measurement of Actual Performance

Once the standards are fixed, the next step is to measure the actual performance. Generally, it is conducted by the managers to analyse the overall efficiency level of the employees. While measuring the performance, objective and reliable methods should be used, such as sample checking, preparing reports, personal observation, etc.

Measurement should be done after the task is completed. However, sometimes performance can be measured during the performance to ensure regular control over the activities. Usually, in large organisations, certain pieces are checked at random, instead of checkisg the whole lot. This is called sample checking.

2. Measurement of Actual Performance

Once the standards are fixed, the next step is to measure the actual performance. Generally, it is conducted by the managers to analyse the overall efficiency level of the employees. While measuring the performance, objective and reliable methods should be used, such as sample checking, preparing reports, personal observation, etc.

Measurement should be done after the task is completed. However, sometimes performance can be measured during the performance to ensure regular control over the activities. Usually, in large organisations, certain pieces are checked at random, instead of checkisg the whole lot. This is called sample checking.

3. Comparing Actual Performance with Standards

This step involves comparison of actual performance with the standard. Such comparison helps in revealing the deviations between actual and desired results. Comparison becomes easier when standards are set in quantitative terms.

4. Analysing Deviations

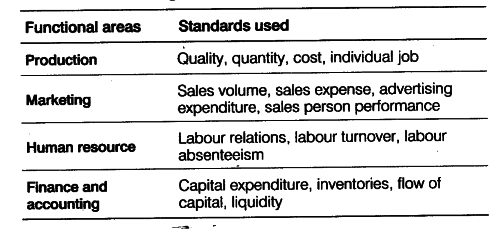

Under this step, deviations in key areas of business need to be attended on urgent basis as compared to deviations in certain insignificant areas. There is a need to determine the acceptable range of deviations in all operational areas. Following points should be kept in mind, while analysing deviations:

(i)Critical Point Control

According to this principle, control system should first focus on Key Result Areas (KRAs) which are critical to the success of the organisation. It is because, it is not possible to keep a check on all the activities of the enterprise. Therefore, if anything goes wrong at the critical points or key areas, immediate action should be taken. e.g. A 5% increase in labour cost is more critical than a 20% increase in postal charges, as 5% increase in labour cost will affect profitability.

(ii)Management/Control by Exception

It suggests that, if manager tries to control everything, he may end up in controlling nothing.

Thus, in this context, it is stated that managers should first handle the deviations, which are beyond the specific range and he should not waste his time and energy in finding solutions of minor deviations, e.g. 2% increase in labour cost is acceptable range of deviation. If the labour cost exceed beyond 2%, immediate action should be taken.